Weekly Gauge #42 : Vote Incentives Price - Part 2

Fixed vs Variable rates

Recap : In the part-1 of this mini-series on vote incentives, we have introduced the economic principles (or flywheel) at play within the governance wars, and identified several variables that are responsible for the correlation between the volume and value of incentives.

Even though they are non-transferable, governance tokens based on gauges tokenomics can have their utility traded like any classes of crypto-assets, in two ways :

Order book based or fixed-rate marketplaces, such as Paladin Quest, allows buyers and sellers to meet at a desired price, encouraging coordination and ev+ situation for each participants,

Free markets or variable-rate marketplaces, for example, Redacted HiddenHand, are more similar to auction structures where the participants' simultaneous behaviors will define the market price.

This article brings together the thoughts, tools, and elements needed to define the scope of voting incentives participants and the behavior patterns and habits of voters in governance wars. We will again refer to the Curve/Convex ecosystem since it has a more disparate shareholding than the others.

Fundamental differences

Variable-rate can be compared to pvp between participants within each side of the market, it is the perfect expression of game theory on governance wars, forcing the local shop to compete with the multinational with a large budget. Some players like Frax can overpay votes because they offset the cost with other cash flows, while some smaller players need to sustain a certain ROI.

The fixed-rate method, although it is less fancy for voters because it reverses the relationship and gives back to incentive distributors the ability to define a fair $/vote ratio, still presents several long-term benefits that strengthen their commitment to voting incentives as well as the votes stickiness.

Role of delegation

Delegation addresses can accumulate a huge control over gauges meta governance, which they hopefully use to flatten the average price but which could in fact let a great standard deviation between incentives because of the inherent conflict of interest of delegators.

Some individual actors like Humpy on Balancer ecosystem also play an important role, although they might accept OTC deals at fair prices relative to underlying emissions controls, their dominance over the governance can influence the market price, thus the bribers’ ROI.

Anticipate vote allocation and define the unknown part

Voters profiles are characterized by different ambitions,

Project or Individuals willing to accumulate a specific token through voting incentives, these are very sticky votes no matter the $/vote ratio as long as they have ev+ strategy in keeping their votes.

Projects owned governance power, mostly used to direct liquidity towards native token pools and POL farming. Behavior aligned with governed project’s growth, accumulating long-term exposure.

Retail governance activist, profit-driven farmer who tries to maximize their $/vote ratio, mercenary capital which dilutes the highest ratio and ignores the lowest, contributes to reducing the standard deviation.

Delegation address, market makers equivalent with a variety of strategies. Focused on aligning emissions distributed with high fees generating pools or specialized on MEV/arbitrage of voting incentives.

Simulate unknown part dilution pressure and start shaping an expected $/vote range

Once we have characterized the personae of governance wars participants it is possible to perform some market intelligence and collect all useful data for our calculations.

On Curve/Convex ecosystem the numbers are the following :

It is possible to use several analytics websites such as LlamaAirforce, Votex, DeFiwars, specialized in gauge tokenomics ecosystems, to gather enough information to formulate educated assumptions about the future distribution of votes and thus the various incentives' final $/vote ratio.

98% of veCRV votes are casted according to Dune Query

Convex owns 50% of all veCRV ; Votium delegation capture 30% of all vlCVX which equates to 15% of total veCRV

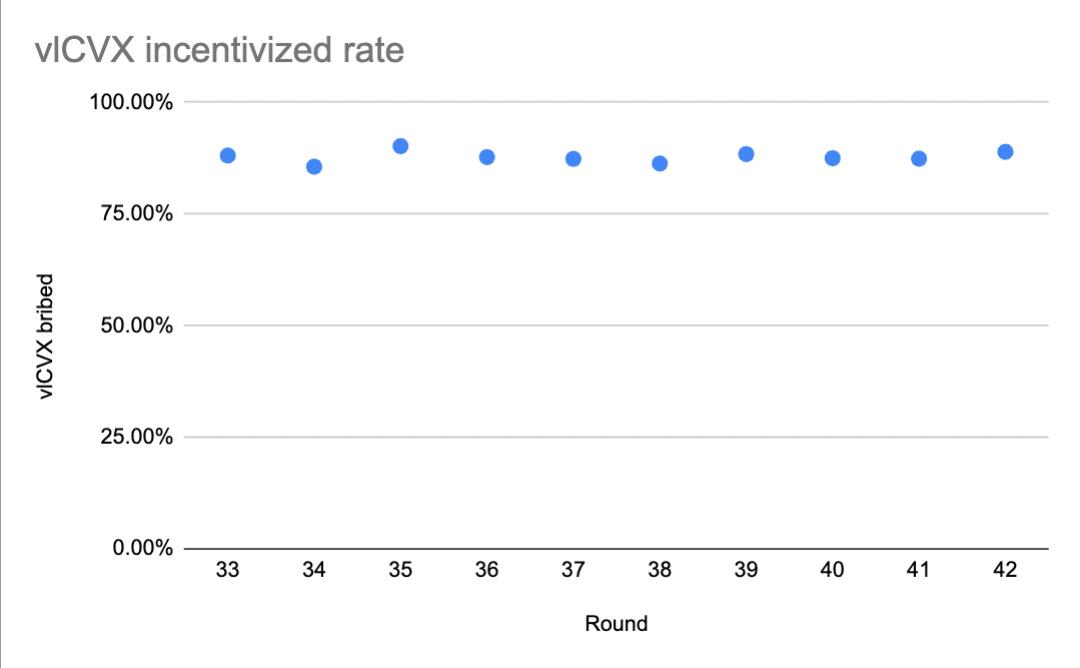

87% of all vlCVX votes toward incentivized gauges, which equates to 251.1M veCRV (44%)

Underlying those vlCVX, 66M veCRV (12%) are owned by protocols to bootstrap their native liquidity including Tokemak, Olympus, Frax, Reserve… Etc etc, you can refer to the CVX Leaderboard and compare the gauge vote results to the respective holdings of each project to confirm it.

Note that most of them actually dilute their own voting incentives and create a hard floor on the $/vote ratio.

93M veCRV (16.2%) are owned by Curve’s founders and casted in tricrypto and 3crv gauges, which they also incentivize every round.

Convex founder c2tp also owns over 5% of veCRV supply in the form of vlCVX, which he uses in a mercenary way to capture voting incentives, with no particular pattern except a focus on highly liquid pools and voting incentives offering the same reward token.

27M veCRV (5%) owned by Stake liquid wrapper are used in partnership deals to vote mostly for 3crv and CRV-ETH gauges as well as Wonderland mim-3crv and Synthetix sUSD and sETH pools

62M veCRV (11%) owned by Yearn liquid locker $yCRV, are used in the same way as StakeDAO’s to vote for a known set of gauges according to partnership deals such as AIP-9 with Abracadabra.money. Lastly, they concentrated 20M votes towards the Tangible USDR gauge.

Predictable votes then represent the sum of the veCRV supply whose votes are identified, thus the “volatile” part represents the remaining unidentified votes. In a simultaneous game with the possibility to change strategy until the end, a last-minute unbalancing is likely to occur, its maximum impact would be measured by :

1- ((Total incentive($) for gauge X / (identified votes for gauge X + max unidentified votes)) / Current gauge X ratio) * 100

This could also be expressed by applying the historical standard deviation of incentives to define the limits of the dilution range, a method that we will detail further in the next part of this series.

Moreover, we will see that it is possible to apply many conditions to reduce the max unknown votes quantity for each specific incentive and that all these conditions tend to guide the average $/vote towards an equilibrium price.

In conclusion, the Part-1 of this research hinted that to find the constant in our vote pricing model the best would be to look into voter participation. In Part-2 we have identified several clusters and habits of voters and started to quantify the maximum final price range of a specific incentive. In Part-3 we will funnel toward a more precise answer by adding probabilistic components.

—---------------------------

A broader observation that highlights the diversity of goals within participants of each side of the market suggests that an optimal system would split the free market and fixed rate, to create a healthier competitive environment, which would allow participants to pursue different strategies without unbalancing the said market.