Weekly Gauge #9: Transferability and Locked Tokens

In the previous editions of the Weekly Gauge, we’ve mainly studied the distribution of governance power among projects within the Ethereum ecosystem and the efficiency of cash flows related to it. One topic that we haven’t addressed is the importance of non-transferability of veTokens.

Curve Finance introduced the concept of locking tokens for a certain duration in order to acquire governance power, protocol fees and the monetary value creation of the protocol (emissions). Following its success, a lot of stakeholders started to build on top of Curve or use the same approach to tokenomics. So far, very few have achieved as much success as Curve, Balancer being the runner-up.

Convex Finance was the real game-changer, as they quickly realized that mutualizing veCRV into their protocol, they could become the optimal farming layer on Curve. The goal was to offer a more retail-centric approach to Curve, by maximizing boosts, minimizing gas costs for governance and offering delegation all while benefitting from Curve’s value proposition.

During its whitelisting process in the Curve forums, some believed that making a more liquid wrapper of the veCRV would kill the voting escrow mechanism. This is why vlCVX has a 16 week lock period. After one year of liquidity, we can clearly see it raised the bar on winning actual governance votes because there are much more retail voters on the Convex side who simply are not interested in these affairs. However, it also helped the gauge weight vote blow up, with more than 1500 stakeholders participating in the game of capital allocation, 80% of which are on the Convex layer. This very symbiotic relationship gave birth to a new DeFi native market, the bribe economy (yes, the name sucks, but we have to embrace the memes).

While sounding very controversial when you explain it to your family or non-crypto friends, the process of bribes is more similar to proxy voting in TradFi than actual bribing. By splitting political decisions and capital allocation, Curve Finance revealed that there was significant value for protocols in letting their stakeholders direct emissions.

However, there are still some inefficiencies that need to be highlighted and corrected if we want to preserve the sustainability of this ecosystem for veToken holders.

In term of revenue generation, this emission system incentivizes core team-backed pools, popular pools and the ones who are bribing. The pools actually driving volume, and fees, could be neither of those three. Balancer has launched discussions on this issue, and hopes to reduce potential emissions to non-revenue driving pools.

Most solutions to acquire gauge votes result in arbitrary costs and distribution of rewards. While it is a very good product-market fit to bootstrap pools and generate another layer of yield for the underlying veTokens, our previous newsletters have shown that this current system forces the DAOs paying for bribes (the actual clients making this market function) carry the risk. In fact, a good number of projects are losing money at the end of the day, especially on the veBAL layer.

Making veTokens more liquid is beneficial for the emission management. Blaming them for the decreasing governance participation would be overly critical since most DAOs scaling suffer the same problem.

When distributing thousands, if not millions of dollars of incentive, protocols need to follow a tight financial management strategy which includes the ability to preview and budget income flows. Assumptions and predictions can be made by analyzing historical data. However, the easiest and most important way to manage treasury is by getting fixed rate strategies to ensure a floor of income that covers your spending. Furthermore, this also allow projects to set up enough criterias to build more complex structured products on top of their initial strategy.

Paladin protocol has been specializing in providing tools and has built an extremely composable product. Our dapps allow projects to acquire a minimum of votes that fits their expectations on several layers of the so-called governance wars. These include Curve & Balancer and others like Convex and Aura Finance. On top of that, Paladin has closely followed the delta neutral narrative that emerged recently and has started working actively on hedging solutions for bribers.

Because the DeFi stack should not be a house of cards, let’s build the future of finance wisely.

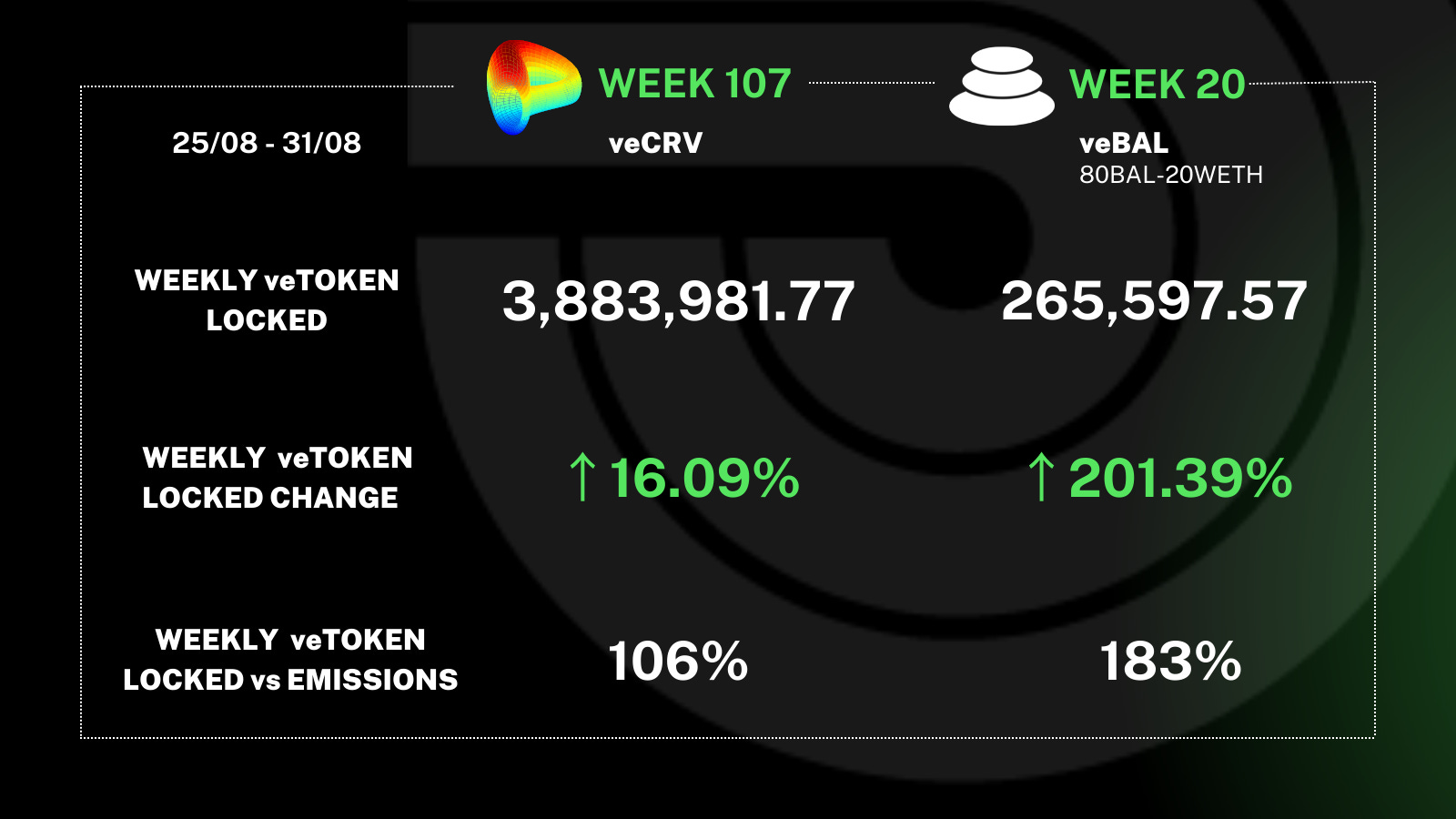

A few last words for our insight hunters. This week the lock rate of both veCRV and veBAL was greater than the emission, which is a very good ratio to measure the sustainability of the system.

Hello Weekly Gauge readers. Have you used our dapp, Quest? We launched a new survey to commemorate the 3 month anniversary launch of Quest and we would really appreciate your user feedback! Limited edition NFTs will be rewarded to users who make a submission. 👉Survey remains open until this Monday, September 5th.