Weekly Gauge #81: Prisma Redemption Arc

Repeg, Reboot, Resupply

Prisma Finance was initially introduced in middle of 2023 as a new DeFi stablecoin primitive, partially forked from Liquity protocol, focused on unlocking the full potential of Ethereum liquid staking tokens (LSTs), and backed by well known builders, ventures, and projects including Convex Finance, where Prisma token products were heavily incentivized since the inception of the protocol.

While the flywheel fueled by Prisma’s veTokenomic and supported by Convex meta-governance experienced a steady growth attracting up to 500M$ TVL and generating about 1M$ in voting incentives over time, an unexpected event will stop the project in its tracks.

Today, the Prisma redemption arc has begun and it’s shaped like a hippopotamus. Let’s take a dive into Resupply, a Convex and Yearn subDAO.

Prisma’s last hours

In March 2024, Prisma Finance announced a system upgrade requiring users of mkUSD (LSTs backed) and ULTRA (LRTs backed) stablecoins to migrate their collateral debt positions (CDPs) from the legacy vault to a new one, allowing for more efficiency and composability for Prisma assets within DeFi.

A vulnerability in both versions of the MigrateTroveZap (mkUSD and ULTRA) contract of Prisma Finance led to a loss of 3,479.24 ETH, or approximately $12 million USD. More details on the hack can be found here.

Interestingly enough, mkUSD and ULTRA stablecoins retained their peg within an acceptable 2-3% range, and continued to generate revenue to flow to stakers, which -considering the context- highlighted a good foundation to support a great rebuilding.

As a result, and despite the core protocol contracts were not affected by the exploit, Prisma protocol has been paused for an extended period of time, in parallel with efforts to recover stolen funds. PIP-39 and PIP-40 defined the reimbursement plan for affected users at an equal sum of roughly 10 ETH per users, whereas the average loss was 145 ETH.

As highlighted by Winthorpe in PIP-46, following the hack the protocol never truly recovered, moreover the project’s github repositories activity show that devs activity greatly decreased. As such, a proposal to shutdown Prisma Finance was submitted to the community, presenting by the same occasion a successor to the protocol, under Convex and Yearn flags, Resupply Fi.

A new Convex and Yearn subDAO

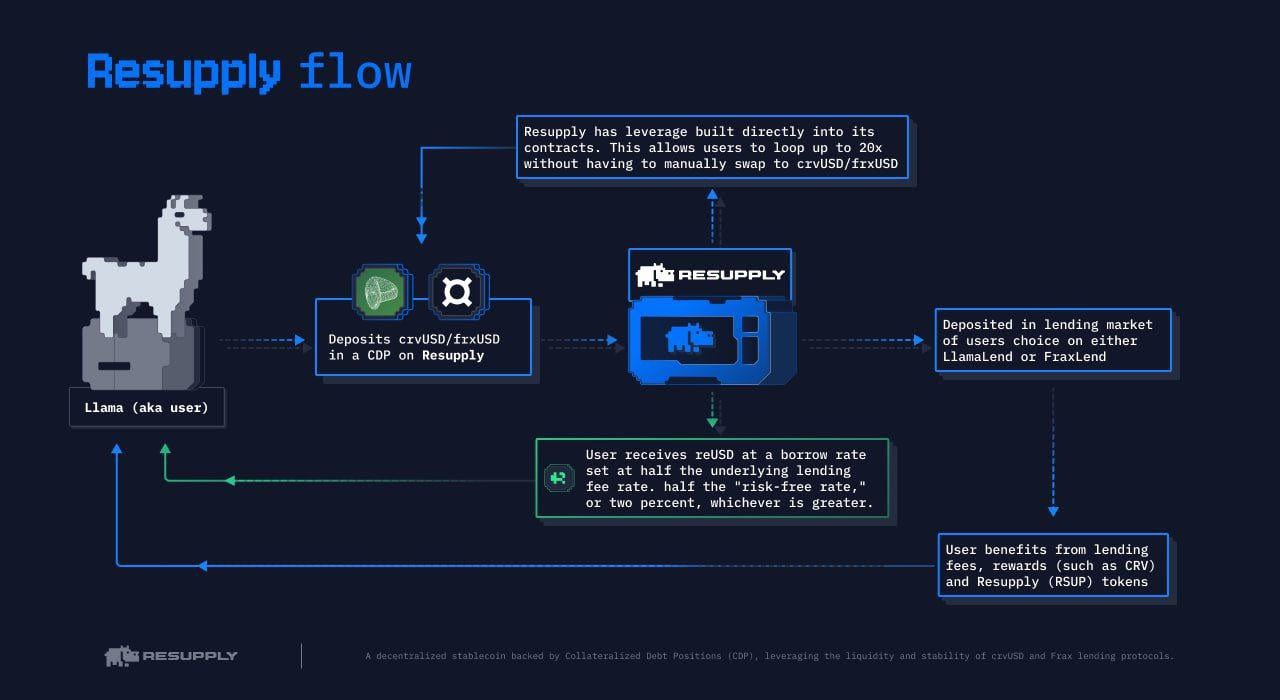

Built upon the FraxLend codebase, ResupplyFi was introduced in December 2024 as a stablecoin protocol succeeding to Prisma, issuing the reUSD backed by crvUSD and frxUSD, as well as a new native governance token RSUP.

reUSD harnesses the fundamentals of the restaking primitive, basically rehypothecation of assets, mixed with yield-bearing stablecoin lending, to offer a multi-level reward structure while capturing fees to redistribute to RSUP holders (in proportions defined by governance).

In continuity to the role played by cvxPrisma in the Convex ecosystem, even though the timelock component of PRISMA vetokenomic is replaced by an unstaking cooldown on the RSUP token, ResupplyFi is a clear value driver to the CVX token.

For more context to how it impacts the ecosystem as a whole, we know as Curve Finance crvUSD supply increases, borrow rates are pushed down. As users mint crvUSD (to deposit & loop on @ResupplyFi), the demand for CRV is boosted by the increased fee generation, which then encourages users to access veCRV via Convex vlCVX to earn those fees.

In short, CRV's value increasing positively impacts voting markets, further encouraging DeFi protocols to pursue revenue drivers (ie, incentivizing their pools via voting markets).

A brighter future ?

Prisma evolution into Resupply, beyond a simple rebranding, introduces technical and economic improvements to the protocol design ; however, the migration of PRISMA tokenomics toward RSUP have raised questions relative to the fairness of migration parameters for legacy token holders.

As proposed in PIP-46:

“Turn in your Prisma, cvxPrisma, and yPrisma tokens for a vesting allocation of RSUP.”

“For locked vePrisma, there is a penalty enforced when locks are broken. To encourage users to break their locks, an airdrop will be created to award users with the amount of RSUP corresponding to the lock break penalty they incurred.”

Community concerns about the forced vesting of PRISMA migrators, and artificial pump of the token valuation via the launch of RSUP token, tends to alert about the consideration for historical holders and users of Prisma Finance.

In conclusion, ResupplyFi is a promising protocol built under experienced teams advisory and upon solid foundations. It will be interesting to monitor the outcomes of the tokenomic transition related proposals, to assess the potential of the RSUP token, especially for the OG PRISMA holder community.