Weekly Gauge #74: What’s DeFi

Hot topic

DeFi initially emerged as a set of financial services built on blockchain technology, adhering to a core set of technical criteria: permissionless access, non-custodial asset management, and the use of smart contracts to automate transactions. Yet, as DeFi applications gained popularity, the term began to stretch beyond its original scope, becoming a mainstream label for nearly any smart contract-based application.

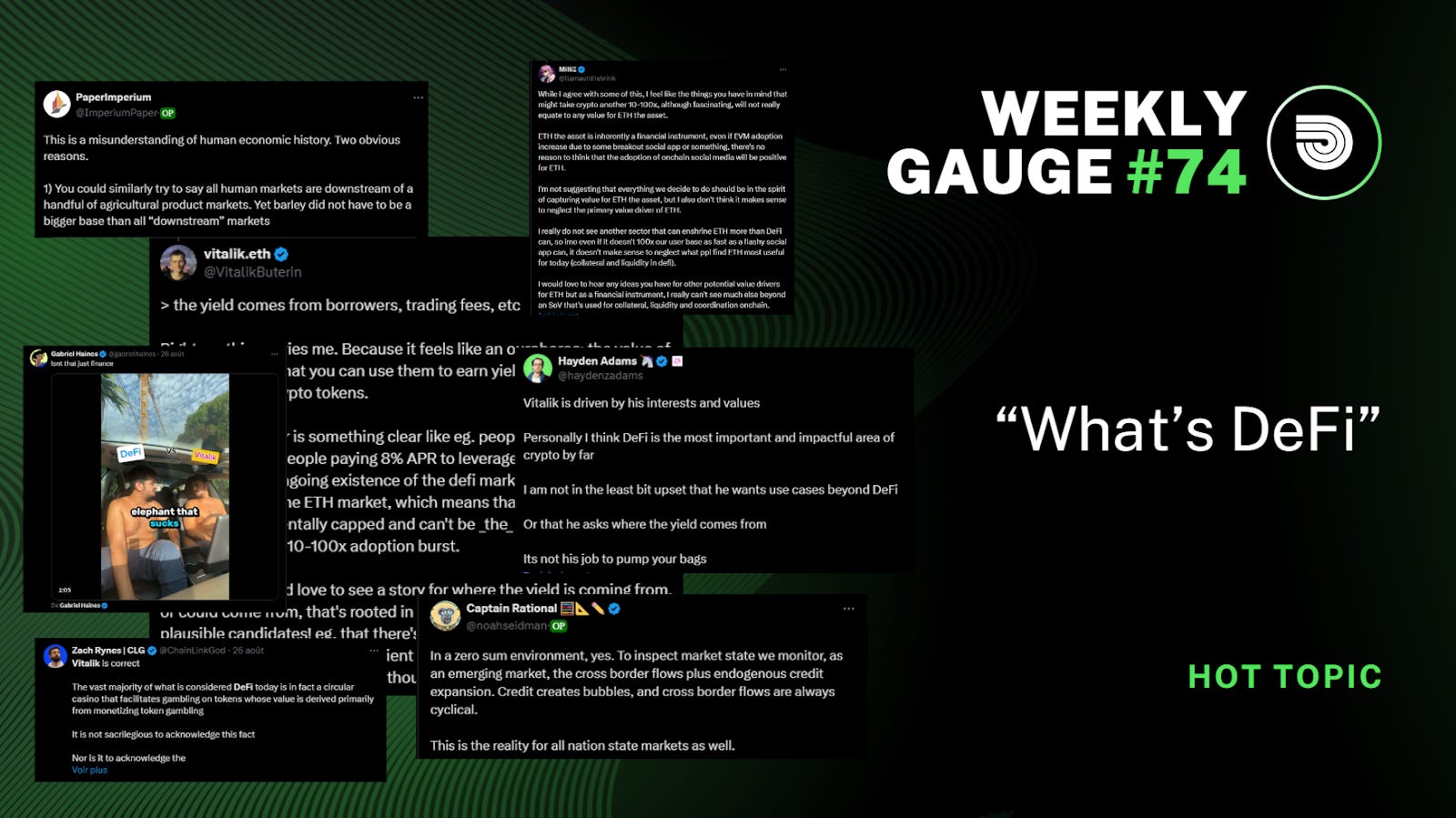

Recently, Ethereum co-founder Vitalik Buterin voiced concerns over the evolving definition of DeFi, arguing that much of what falls under this term today strays from its foundational principles and faces inherent scalability limitations. In this article, we’ll trace DeFi's origins, explore the reasons behind the debate over its definition, and discuss why the focus should remain on addressing core challenges rather than getting caught up in semantics.

DeFi 1.0 vs 2.0

DeFi evolution follows cycles that impact market dynamics, we can describe how previous ones did and anticipate how the future will do.

1.1 Roots (on Innovation):

While presenting substantially more efficient, secure, and transparent fundamentals, the first crypto currencies use cases remained very niche and the adoption limited. The creation of programmable application layers such as Ethereum later enabled the development of a wider scope of primitives inspired by traditional finance e.g AMMs or stablecoins, but also the first DeFi native use cases such as flashloans by AAVE. Innovation alone is not guarantee of success, it requires to solve a common issue and be accessible without advanced knowledge of the underlying mechanisms.

1.2 DeFi Summer macro (on Adoption) :

External factors can impact the demand by the world for crypto assets, as an alternative financial vehicle, but at scale for its mainstream use cases. The 2020-21 Covid crisis and lockdown, start of Russia war against Ukraine, and record US$ printing, were all catalysts to the propagation of crypto alternatives to real world paused markets or industries. Hence the adoption of DeFi by the next 10-100x users will not solely come from crypto innovation but also from a simultaneous world scale -as opposed to geographically isolated- need.

1.3 Ponzi farms era (on Euphoria):

Extreme catalysts to crypto growth, when there is no proper regulation to crypto activities, and very low education on the inherent risks, will every time ultimately result the way it did (ponzi, rugpulls, order book spoofing).

1.4 Scale the ecosystem (on Liquidity)

The more balanced the capital in and outflows compared to the liquidity depth of DeFi applications, the more sustainable the growth.

The recent all-time high in stablecoin market cap represents a clear indicator of increased on-chain activities participation and adoption. Stablecoins, being a primary on-ramp for new users and capital in DeFi, support the observation that more individuals and institutions are entering the space.

Moreover, the combination of rising open interest and shallow order books suggests that while more traders are entering or maintaining positions, there is not enough liquidity to support significant trading volume without impacting prices.

Loans vs CDPs, UX for a normie

When asked his opinion about AAVE, Vitalik highlights (see https://x.com/VitalikButerin/status/1827579479780180259 ) that most “lending” markets in DeFi are in fact leverage derivative products based called collateral debt position (CDP), and the UX of such products is not what a normie would expect when talking about loans, which is true to some extent, but on the other hand he also says RAI is a great form of decentralized stablecoin although this also isn’t what a normie would expect when talking about a stablecoin.

Andre Cronje in his latest article Why DeFi ? reminds “to protect the IOU’s, the man needs to give the deed to the land he buys as collateral” and “Interest (or yield) on lending is, apart from labour and goods, one of the purest forms of income. There will always be those that need capital to start a new venture, or those that have hard times and just need some help bridging the winter. This type of income is infinitely scalable and pure, it does not rely on any fake incentives”

One lesson to learn here on onboarding normies, is that a common characteristic of every successful DeFi project is their ability to offer sophisticated financial vehicles on simple UIs that remove all the complexities for the end user.

Dexs and stablecoins dominance

So far, putting aside the lending topic, two categories of DeFi products have emerged as essential primitives for any network, Dexs and stablecoins. Recently, a third category is rising comprising both LSDs and LRTs that represents the financial mechanism of rehypothecation.

are these applications (i) useful in a sustainable way, and (ii) don't sacrifice on the principles (permissionlessness, decentralization, etc) ?

DEXs like Uniswap and Curve Finance have become fundamental to DeFi by staying true to principles like permissionlessness and decentralization. These platforms introduce innovative market-making models, are built upon sustainable fees structures, and are pioneers in on-chain community-driven governance.

Stablecoins, while undeniably useful as a medium of exchange and collateral, have their adherence to core DeFi principles varies according to a trilemma between stability, efficiency, and centralisation ; this impacts a lot the chances of having one ultimate stablecoin respecting all the core principles and being accessible to normies, however institutional grade investors can burst a 10-100x growth of the market value wise -as opposed to unique users-.

Scalability matters

5.1 A closed loop

Answering further comments about the duality of his promotion of centralized and gambling like applications as opposed to his description of DeFi like a bunch of short termed farms ; Vitalik states that “the value of crypto tokens is that you can use them to earn yield which is paid for by... people trading crypto tokens.” and “the ongoing existence of the defi market is downstream of the existence of the ETH market, which means that while defi may be great it's fundamentally capped and can't be _the_ thing that brings crypto to another 10-100x adoption burst.”

https://x.com/Togbe0x/status/1827354944564850987

5.2 CT answers :

https://x.com/noahseidman/status/1828046771219501283 ; NoahSeidman highlights the importance of cash flows and credit to assess the market potential, this echoes to 1.4, the stability of DeFi yields can be sustained by applications downstream of ETH. Furthermore, value can be captured from other networks liquidity e.g BTC wrappers as we explained in Weekly Gauge #73.

https://x.com/ImperiumPaper/status/1827838667588595990 ; ImperiumPaper highlights, through a social experiment story, that the utility you give to an asset can change its perceived value and hence an extra can be created from a finite base of assets. Hence the uncapped potential of DeFi relative to its underlying exchange medium.

On a lighter note I would like to highlight that NFTs, that is a purely DeFi native product, and despite that it started out as a spectacular bubble (refer to 1.3), is whatsoever a DeFi innovation that generated a 10-100x adoption burst.

In conclusion, while debates about definitions and semantics will continue, the real challenge lies in ensuring that DeFi remains accessible, transparent, and resilient, even as it grows. Whether through the simple integration of traditional products or the exploration of entirely new paradigms, the focus must remain on delivering tangible value to users, bringing us closer to the future of France.