Weekly Gauge #60: Both sides of the Curve

The $CRV equilibriums

2023, as the Chinese year of the rabbit, has burrowed into a downward spiral symbolized by a market downturn and a year dedicated to laying foundations. 2024, the year of the dragon, looks about to take flight promising a market renaissance. Nevertheless, the llama, forever excluded from the zodiac, faces the ominous prospect of being devoured by the soaring dragon of fortune.

vlCVX bribes efficiency

The round 63 of vlCVX vote incentives highlighted the previously established direct correlation between total volume of incentives available and the resulting $/vote on variable rates based marketplaces such as votium, with a decrease in overall value of around 30% resulting in a 28% down change in average $/vote. While this helped Votium overall performance to regain net positive levels for the incentive creators, it still demonstrates the saturation of the platform capacity to handle new entrants diluting historical users performances. This is most likely due to the Votium delegation address voting power remaining flat hence diverging from the overall incentive value uptrend, thus breaking the previously achieved equilibrium.

In the dynamic of governance markets, voters seek a higher value per vote, while bribers aim for a lower cost per vote. Hence the value of votes naturally trends toward an equilibrium between voters and bribers expectations, by leveraging the competition between Votium and Quest marketplaces. When bribers overpay on Votium, their attention shift to Quest, resulting in a dilution of the value per vote for Votium. This dilution occurs because of the correlation between total value of incentives available and quantity of votes to be casted. Since Votium delegation address does not participate in multiple marketplaces, part of the delegators should naturally arbitrage the difference in $/vote rates between both marketplace due to the migration of bribers, by changing their delegation to Paladin auto voter. This action leads to a convergence of the average value per vote between Quest and Votium, achieving equilibrium between voters and bribers, the governance (3;3).

We can observe from the chart above that Paladin Quest vote incentives have consistently achieved a net positive efficiency. This is no sorcery but simple math based on the very user oriented design of the platform, enabling creators to set up either fixed rate or $/vote ranges of incentives following recommendations provided by the team, and redirecting the potential unspent rewards depending on the fill rate of the fixed rate incentives. At the end of the day, better do LM at 1x efficiency rather than overpaying votes compared to the emissions it captures.

Considering the upcoming yearly reduction in CRV emissions rate as well as the historical negative or flat price action of the token, we can anticipate that the threshold of efficiency in $/vote for incentive creators will lower accordingly, thus reducing even more Votium capacity to handle the increasing or even flattening demand for veCRV and vlCVX votes.

Mich OTCs:

Sell rate

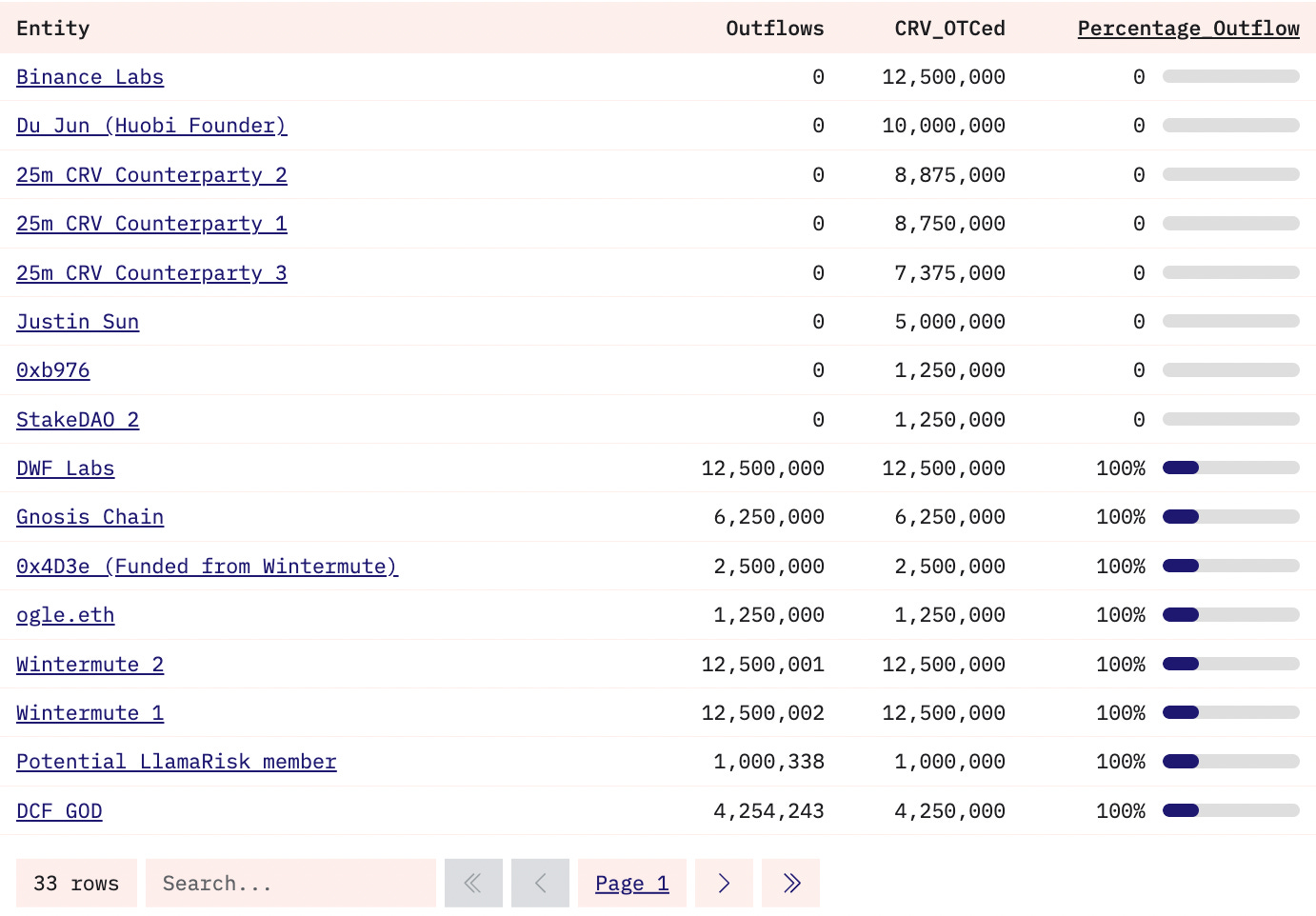

Out of 300M CRV sold by Mitch only 55M have not been sold, which corresponds to approximately 18% of hold rate, this explains the current CRV price action, displayed in the next bullet point against ETH.

Price impact

Llama lend:

On a more positive note, the upcoming addition to the Curve ecosystem, LlamaLend, will serve as Curve's lending platform and is expected to positively impact the ecosystem for several reasons.

Firstly, it promises to significantly boost $CRV revenue by introducing a new product that exclusively utilizes $crvUSD. The adoption of $crvUSD is likely to drive its demand, stabilize its peg, and contribute to lower borrowing rates, increasing $crvUSD supply more than new collateral markets would.

Saint Rat's tweet underscores that, assuming stable numbers post-August 2024, Curve will become profitable with a $veCRV fee APY surpassing $CRV inflation. LlamaLend is expected to further boost the $veCRV fee by introducing a new fee-generating product and acting as a crvUSD 'black hole,' which should enhance Curve's profitability.

For a more detailed analysis of Llama Lend's potential impact on CRV's price, insights from wwpk are available.

Secondly, LlamaLend's soft liquidation feature is designed to reduce, though not eliminate, the contagion risk for large loans, such as those by Mich. In soft liquidation, collateral may convert to crvUSD if its value decreases, with a chance for partial recovery if the value goes up, albeit probably less than the initial amount. In worse scenarios, 'hard liquidation' could completely eliminate a position.

This is the last piece of the puzzle enabling Curve to maximize revenue from the billions of TVL it has accumulated.

yCRV :

Back in December 2023, during a regular fee token conversion process on behalf of Yearn's treasury, a faulty multisig script has caused the sale of Yearn-owned yCRV liquidity. The entire balance of 3,794,894 lp-yCRVv2 tokens was swapped instead of just the earned fees. This amount comprised a large portion of the Curve pool (48.5%), and therefore incurred a significant slippage on the trade. The position was strictly protocol-owned liquidity (POL) belonging to Yearn's treasury and it did not contain any user funds.

After addressing the treasury script problem, the yCRV buybacks have been successfully executed. The new staking features are currently undergoing an audit. The audit for the YearnBoostedStaker contract is nearly finished, and is deemed to be upgraded to enable a governance and stablecoin elections feature within the Staker system.

By integrating with Llama Lend from day one, yCRV has the potential to become the first auto compounding crv asset available for borrowing. This early mover advantage could significantly enhance its attractiveness, driving up demand for the locker and supporting the peg.

Overall, 2023 proved to be challenging for Curve for technical and operational reasons highlighted by either Curve’s founder Mich CRV loans default and resulting OTC deals hurting $CRV price action, Votium fundamental inefficiencies, or the yCRV treasury script issue that ended up in a large depeg of the wrapper. Nevertheless the recent efficiency improvements in vlCVX incentives (especially those of Paladin Quest v2) and the positive prospects brought by LlamaLend to the Curve ecosystem, highlight the potential for growth and stability in the year ahead.