Weekly Gauge #46 : A New Stablecoins Era

The rise of lending oriented stables

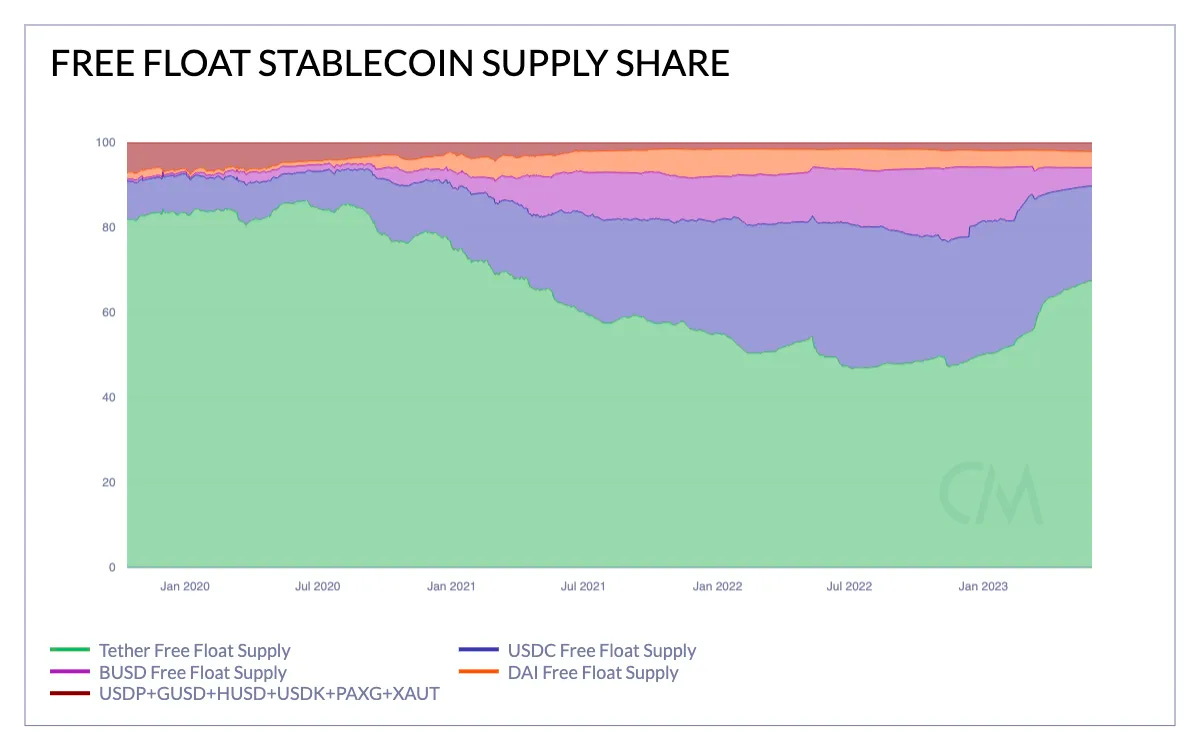

For many years, centralized stablecoins have enjoyed an upward trend in adoption and persisted to take the lion’s share of this market as highlighted in a recent tweet from Bankless HQ.

https://twitter.com/BanklessHQ/status/1664604198821072896

However their future dominance remains uncertain. So far, decentralized stablecoins faced a barrier to exponential growth due to supply caps implemented for security purposes but the new features and enhanced efficiency brought by them could lead to great changes in paradigm on this asset class.

It is essential to remember the risks inherent in algorithmic stablecoins, as demonstrated by the collapse of Luna and other experiments. However, it is crucial to note that this iteration of DeFi stablecoins is not their final form. Continuous advancements and improvements are being made to enhance their stability and resilience.

https://twitter.com/BanklessHQ/status/1664604190013034497

The regulatory landscape surrounding stablecoins is rapidly evolving. Recent lawsuits filed by the Securities and Exchange Commission (SEC) against Binance and Coinbase for their investment vehicles have led to market dumps and highlighted the resiliency that decentralization offers. Assets not listed on centralized exchanges (CEX) demonstrated better price action following the news, emphasizing the advantages of decentralization.

Over-collateralized loans, a common mechanism in the stablecoin market, suffer from fundamental inefficiencies. Market, technology, and operational risks arise from locking funds as collateral on lending platforms. Liquidation events involving large asset holders can lead to market fluctuations. Additionally, liquidators selling collateralized assets can cause the price to drop further, triggering subsequent waves of liquidation. Furthermore, the lack of liquidity on exchanges can result in bad debts for lending platforms, leading to impermanent losses for users who are liquidated.

This article aims to introduce a new generation of decentralized stablecoins specifically designed to meet the needs of the lending market.

Improvements of Liquidation Mechanisms

Collateralized stablecoin architectures always incorporate a liquidation mechanism to safeguard against collateral value depreciation.

The core idea behind crvUSD is an Automated Market Maker (AMM) for continuous liquidation or de-liquidation. Collaterals fluctuate between conversion to $CrvUSD and reversion to the collateral asset based on the price of $CrvUSD relative to $1. With LLAMMA, only 1% of collateral is lost if the price drops 10% below the liquidation threshold and subsequently rebounds.

Remarkably, it took just over a week for crvUSD to approach its initial "debt ceiling" of 10 million units minted, accumulating significant liquidity in its stabilizer pools.

Another example of the crvUSD efficiency :

https://twitter.com/DefiMoon/status/1665767982386098179?s=20

However some users noted that you can’t borrow against CVX on LLAMA, making it not really a fair comparison.

Novel mechanism for stablecoins loans efficiency

The efficiency of stablecoins loans can be significantly enhanced by utilizing yield-bearing assets as collateral to mint Curve’s $crvUSD or Aave’s $GHO. This allows users to continue earning yield and offsets the inefficiencies of over-collateralization. The next step in improving collateral efficiency is accepting LP tokens of pegged assets.

Additionally, the introduction of GHO flashminter creates new use cases for MEV traders and arbitrageurs, who play a crucial role in maintaining the stablecoin's peg. Tapioca's USDO stablecoin also offers similar features, making them competitors in this sense.

https://governance.aave.com/t/arfc-gho-mainnet-launch/13574

The importance of multichain

Tapioca's USDO, an omnichain stablecoin available across 17 chains, utilizes LayerZero's generalized messaging network to eliminate the need for bridging. As a result, users can mint, borrow, and lend USDO seamlessly across any chain supported by LayerZero.

$USDO uses the LayerZero OFT V2 token super standard. OFT stands for “omnichain fungible token,” and completely removes the need for traditional bridging. With USDO using this standard, it can mint and burn from chain to chain in an instant, even from an EVM to a non-EVM chain!

In conclusion, decentralized stablecoins offer a promising alternative to centralized counterparts. With ongoing improvements in design, regulatory considerations, and collateral efficiency, these innovative solutions aim to provide enhanced stability and resilience in the lending market. As the decentralized finance ecosystem evolves, the future of stablecoins looks poised for continued growth and innovation.