Weekly Gauge #45 : Fees & Alignment with Gauge Tokenomics

veBAL case study

The concept of real yield for Defi users represents the actual returns after taking in account all of the costs associated with investing, including fees, gas costs, and impermanent loss. The concept is also used to define yield that is not relying on protocol’s native token emissions, in other words it represents actual value creation for the users.

Fees are an important part because they help to ensure the security and sustainability of a protocol, they are often used to pay for the costs of running the protocol, such as developer salaries and marketing expenses. However, in order to incentivize deposits and liquidity depth of their pools, most protocols implemented a fee sharing mechanism.

In this article, we will analyze how LP based gauge tokenomics can improve this mechanism and strengthen the revenues for both protocols and users.

Defi gauge tokenomics that relies on LP token locks, such as Balancer, helps to create a more sustainable fee generation model. By locking up their share of the pool, liquidity providers are effectively committing to providing liquidity to the protocol for a period of time. This helps to reduce volatility of the protocol’s fees, making it more attractive for new users.

On Thursday, April 7th ‘22 the on-chain liquidity mining system (or veBAL gauge tokenomic) kicked off for Balancer, since then we can observe a significant increase in fees generated on the BAL-wETH pool.

Note that 75% of all fees generated by the protocol are proportionally distributed to veBAL holders. However a specific distribution scheme was defined to allocate those fees in a way that further align veBAL holders with the project’s growth.

For pools designated as Core Pools these fees are paid out in the form of USDC incentives placed on voting incentive marketplaces which can be earned by veBAL lockers by voting on the pools that generate these fees.

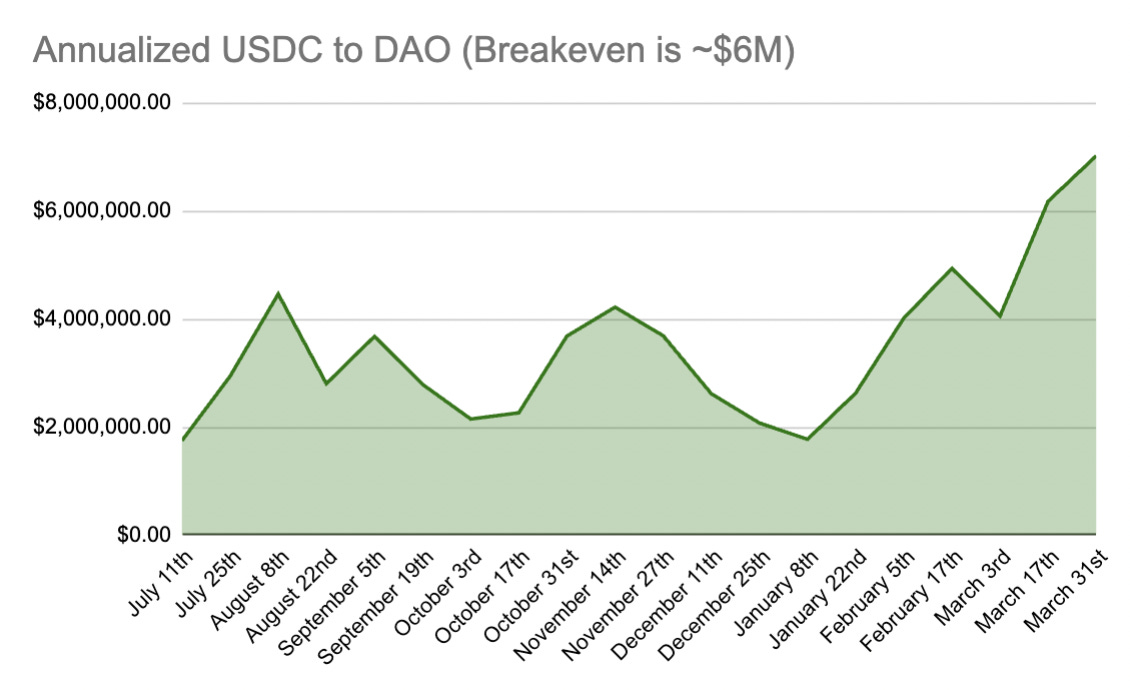

We can observe in the above chart that USDC to DAO recently crossed the breakeven threshold, which confirms the efficiency of the current distribution model.

For other pools (no yield bearing component or exceptions for ve8020), these fees are paid out as claimable rewards for veBAL lockers. In this case, all BAL is paid out as BAL, and all other tokens are currently sold for bb-a-usd and paid out as such.

Last week, the fee token distributed was changed from bb-a-USD v2 to bb-a-USD v3 (Balancer Boosted Aave V3 USD Composable Stable Pool) due to a reentrancy vulnerability, based on community feedback taken in the Balancer Forum followed by a Snapshot vote in May '23.

The main advantage of such design is that it allows users to passively increase their fee sharing revenue thanks to AAVE interest rates on boosted pools underlying assets.

In conclusion, the veBAL model based on liquidity provision token has several advantages compared to the vanilla gauge tokenomics introduced by curve, that distributes 3CRV tokens as part of the fee sharing mechanism, and feed the flywheel with even more composability and harnessing of users deposited funds.