Weekly Gauge #20 : Voters Coordination Challenge

Exploring the DeFi Stack Interdependencies

Voting incentive is among the most powerful ways of ensuring activism by governance token holders. It can also be among the most challenging, particularly when it comes to allocating sustainable and fair distribution of rewards.

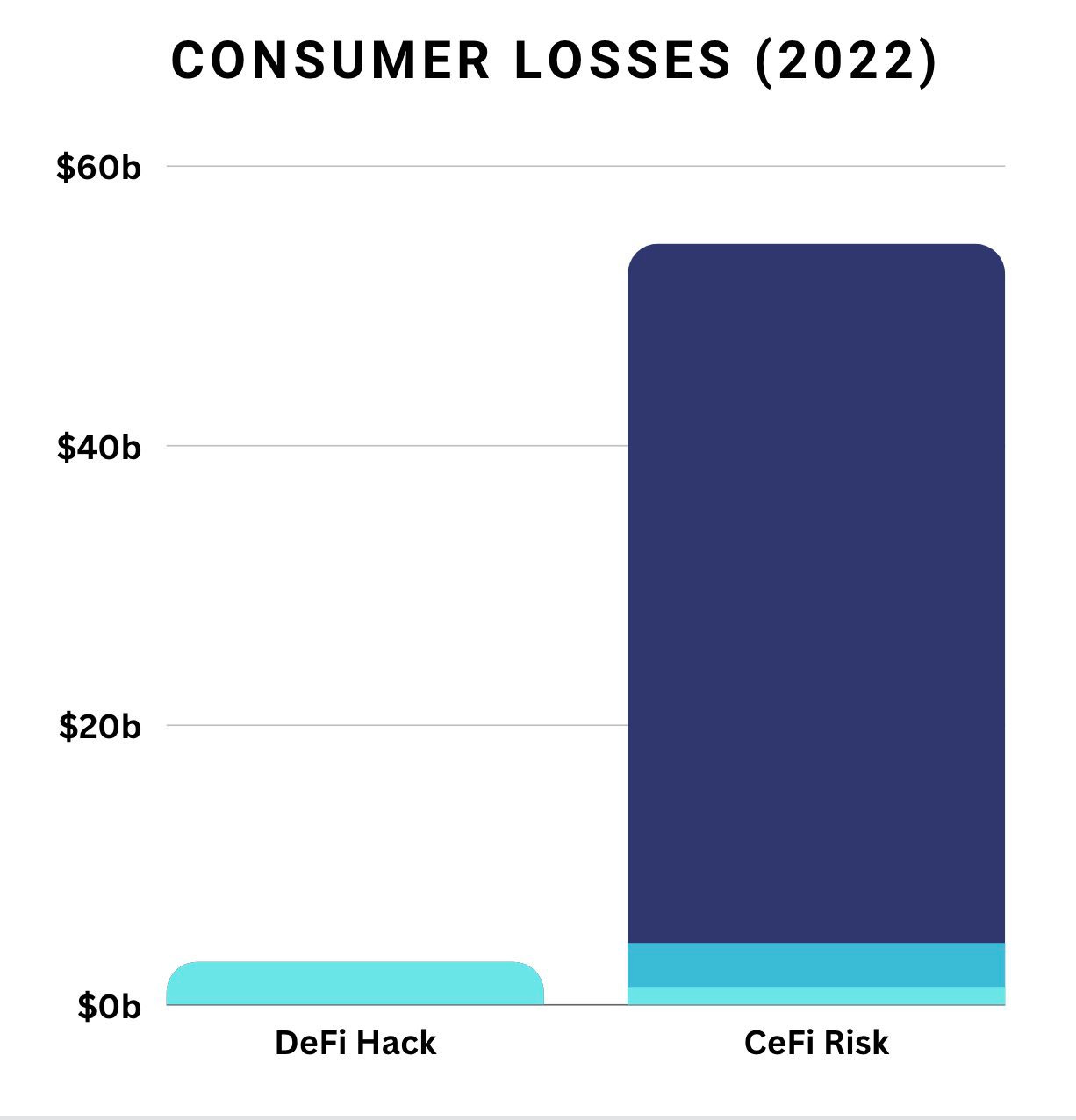

Today, with the decentralized landscape in a state of near-permanent flux and the uncertainty around custodian institutions, the importance of making investors’ voices heard is perhaps greater than ever.

Source : https://twitter.com/QuadrataNetwork

Gauge voting mechanisms pioneered by Curve and implemented by a myriad of protocols have presented a compelling arena in which to demonstrate how a project’s behavior affects the attractiveness of their native token, thus, voters' inclinations to access to the voting incentive.

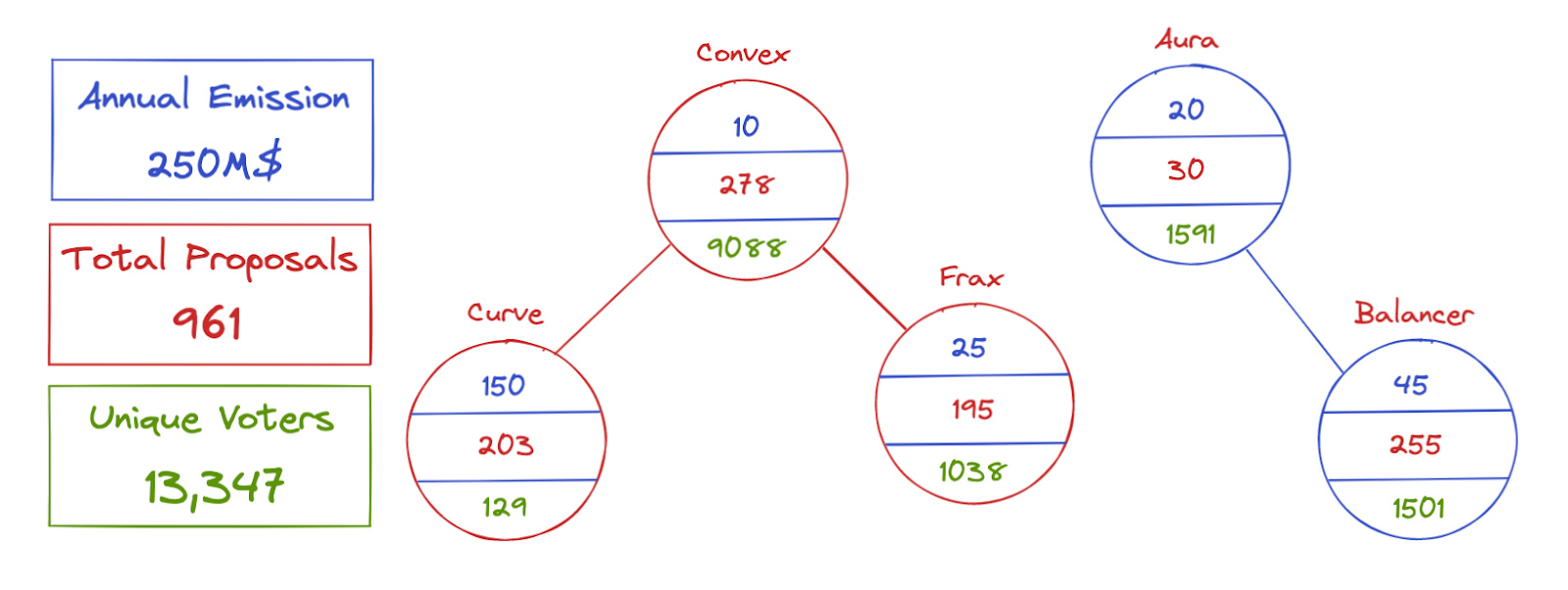

When talking about VeToken ecosystems we can bound our research on two major but still not equally mature clusters. On one hand, Curve and Convex are intimately connected as we can see almost all voters prefer to use the vlCVX layer to direct the CRV emission, allowing them to earn CVX and FXS on top.

On the other hand, Balancer’s most promising liquid locker, Aura Finance, still needs to attract more veBAL to affirm its leadership. In the meantime, competitors like Tetu are acquiring significant market shares, and an adversarial coalition keeps farming 30%+ of BAL emissions on pools of low revenue for the protocol.

2022-2023 Major Emissions Market

If driven by the sole perspective of directing the inflation of the currency he owns, the vetoken holder will eventually adopt a selfish behavior. Moreover, considering that a vetoken holder does not ultimately provide liquidity within any pool of the subsequent protocol, we can assume that the distribution of newly emitted tokens won’t be coordinated nor aligned with the protocol growth.

Fortunately, the DeFi stack rarely leads to a dead-end, as the game theory of such a voting-escrow mechanism strongly encourages projects - operating a part of their services on the platform - to incentivize votes and offer the best yields to attract volume and depth.

In 2022, the voting incentives market generated almost 250M$ of revenue for veholders, this is basically paying voters as much value as they are responsible for and making sure that competition between stakeholders leads to positive outcomes. Eventually, the coordination between voters varies according to the attractiveness of bribed tokens, which often relies on narratives and traders' behavior which creates volume and fees for the base protocol.

YTD Yield Generated by Bribes

Unfortunately, some inefficiencies remain i.e vlAura is currently more expensive than vlCVX on the bribe market (cost 0.04748$ against 0.03551$), paradoxically it captures 0.0195$ of $BAL emission against 0.0242$ of $CRV emission per vlCVX. This event is due to the non-compliant distribution scheme of major marketplace, and can be solved by setting a fixed price for votes according to the project’s needs, using Quest.

The frequency and duration of voting rounds, for example, is concentrated into just a few days, which means the decision-making process is likely to come under time and resource pressures.

Delegation address allows voting power holders to reach informed decisions with the support of both third-party research and in-house expertise, provided first and foremost by the Paladin team.