Weekly Gauge #19: CeFi Collapse Contagion

“It can always get worse” - Yesterday reminded us of the main rule of bear markets.

Despite the spectacular crash of one of the biggest players in both CeFi (FTX) and market makers (Alameda), DeFi somehow managed to hold its head high.

In today’s Weekly Gauge, let’s have a look at the causes and yet foreseeable consequences of such an event on the governance wars’ cash flows and participants.

The rumors regarding FTX's insolvency first started when Coindesk reported that Alameda's assets amounted to $14.6B, out of which $3.66B is unlocked $FTT and $2.16B FTT, were being used as collateral. In light of the uncertainties, Binance's CEO CZ has announced that they would be liquidating the $FTT on their book.

Alameda's CEO, Caroline, has tried to clear the air by stating that there are $10b+ assets in their books which are not reflected publicly. However, the truth of their insolvency eventually came out and, in a totally unexpected plot twist, CZ announced that Binance would be acquiring FTX to help cover the debts:

Following the news, a short upside manipulation then propelled a massive dump on every market, catalyzed by FTT liquidations.

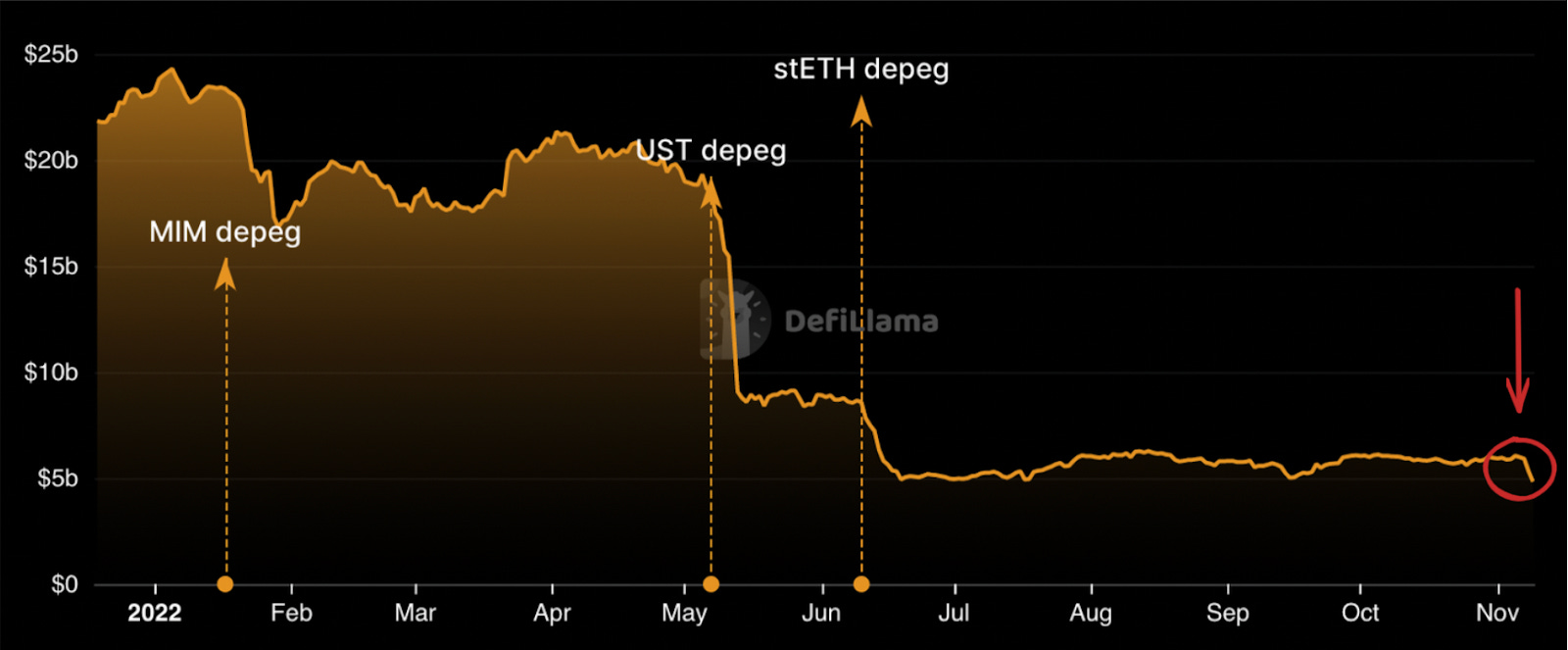

Obviously, there were significant TVL drawdowns, with Curve and Convex losing over 500m$ of TVL, and Abracadabra stablecoin $MIM losing close to 150M$ of TVL.

Paradoxically, this loss of TVL has not affected the efficiency of DeFi in the slightest. As with every black swan, gas goes up but the contracts keep executing, the transparency is intact, and there are no bad surprises. Life goes on.

However, the price impact of this event on Curve and Convex native tokens has strongly depreciated the revenue captured per vote, and thereby, the value of the Golden Ratio for bribers. Moreover, the CVX token has shown better resilience to the crash than the CRV token, which directly affected its mean over the control of CRV emissions from 5.25x to 5.5x.

The aftermath of such an unexpected collapse within the major custodial cryptocurrency exchanges will fatally trigger a wide redistribution of funds among the platforms. In addition, it may strengthen the non-custodial decentralized ethOS, hence, directing user base market shares toward DEXes, such as Curve, Balancer and Uniswap.

An increase in volume on those protocols directly implies an increase in accrued fees and interest, which will result in more revenue shared between users. While most of the tokens are down back to pre-bull run prices, which could lead us to a misleading interpretation that we’ve just made a round trip, it is important to bear in mind that the overall DeFi market cap is still 2.5x higher.

In a year of turmoil, the last 24 hours have been the worst thing that has happened in the crypto space, by order of magnitude. It underscores the need again for transparent, overcollateralized systems that can deleverage in an orderly manner. It ironically underscores the need for crypto.

We are proud at @Paladin_vote to contribute to building such a resilient, sustainable and fair economy, based on active individual participation.