Weekly Gauge #17: Frax Saga Part 1: Bootstrapping Phase

With over 3.9M CVX, Frax is the biggest non core-team holder of CVX - even ahead of wrappers like bveCVX or pxCVX. This lead was not created by a large and sudden market buy. Instead, Frax has made a long-term directional bet on Convex which is paying off exponentially.

Historically, FXS rewards have played a significant role in the development of the bribe market. Frax's strategy to remain the most competitive yield alternative attracted a lot of liquidity to the protocol's pools (over 2 billion dollars at some point). However, this was only the bootstrapping phase of Frax's long-term strategy.

In this article, we will set up the field for future deeper analysis of the bribe incentive framework of FRAX and why the Frax Basepool is a way for them to move onto a diversification phase.

On one hand, we can observe the red area of the chart on the left, which indicates that Frax’s voting incentive program became profitable during the previous round (20/10/2022). On the other hand, we can take the situation under the vlCVX mercenary holders' point of view and observe that they were forced to re-align with the protocol growth by selling their votes at a fair price. However, this doesn’t imply that each pool respectively is incentivized according to the value it captures from Curve Finance.

So, why would a protocol spend more than 80M$ to capture the Curve ecosystem incentive? Initially, this was done to create an extremely deep Frax-3pool pair. This enabled FRAX to have a very strong peg, as well as farming with their USDC collateral (which was used to mint FRAX), via what they called an AMO (Algorithmic Market Operator).

This enabled FRAX users, including the DAO to farm more than 110M$ of CRV & CVX, thus putting FRAX in the position they are in today. Additionally, Frax accumulated voting power very quickly, which enabled them to always recoup a significant part of their incentives, hence not really spending as much as the budget would let people think.

In order to truly succeed as a stablecoin, you need to constantly add a new use to your asset and push protocols to pair with it as a base asset. This is something the Frax time seems to have been prescient on, as they have built their whole success on partnerships. With hindsight, it also seems to be the reason why they went so hard on Curve and Convex.

Now that they own a significant stake in the Curve ecosystem, they can allocate rewards to the pool, deciding to use FRAX as a base asset. This idea materialized as the FRAX Basepool: if protocols pair their token with the FRAX-BP, Frax will create vote incentives with a pro-rata chunk of their revenue to incentivize deposits in the pool.

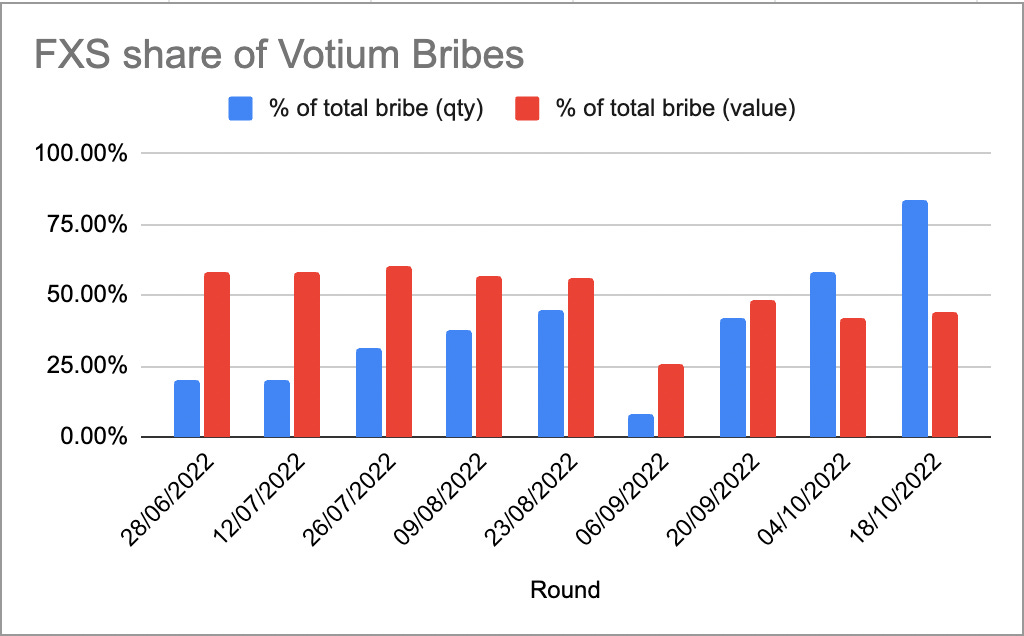

Saying that Frax is the king of Curve might be inaccurate, but we noticed during the past 5 rounds that FXS incentives have been distributed more widely among metapools, making the token responsible for over 50% of Votium cash flows and 80% of the total available bribes count. This diversification comes with a slight correlation to a decrease in $/vote ratio which is a positive sign, as we can see in the graph above.

At Paladin, we believe Frax’s strategy could be more efficient. Curious how this could be done? Tune in next week to find out!