Weekly Gauge #16 : The Gauge Market Maker - Part 2

In order to align the behavior of every stakeholder of the ecosystem, Curve Finance introduced the veCRV governance framework. This model allows long-term holders to direct emissions to the protocol’s users.

Thanks to the veCRV locking mechanism, the composability of Curve protocol has grown, and new actors started to build on top of it which resulted in more market-making opportunities on the governance layer.

In the part one of this article series, we outlined the role played by Liquid Lockers governance within the gauge incentive market. Part 2 will focus on the market-making opportunity created by the secondary market of wrapped CRV.

Curve Finance is a decentralized exchange designed to optimize the trading efficiency between similarly behaving assets, such as stablecoins and wrappers. It appears optimal to run the exit liquidity pools for wrapped CRV directly on that exchange because it creates a flywheel on trading fees. However, the primary reason is because it contributes to the peg of the wrapper token thanks to the stableswap formula of the AMM.

In order to justify their value proposition, Liquid Lockers should be able to provide a 1:1 ratio to traders between CRV and their wrapper. This can be achieved in two ways :

Deep CRV liquidity coming from external providers or by Locker’s POL ; this will allow to scale the market and perform large-sized trades without price impact or slippage.

Hedging mechanisms against black swan market events to strengthen the depositor confidence and traders’ behavior.

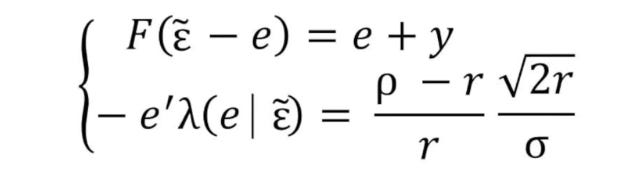

Thanks to Gossner's work in game theory, we were able to model the behavior of liquidity providers and quantify it by the two equations below. These two equations allow us to obtain a differential equation, this one having a unique solution: the equilibrium point, which means that it is possible to provide a prediction based on the theory.

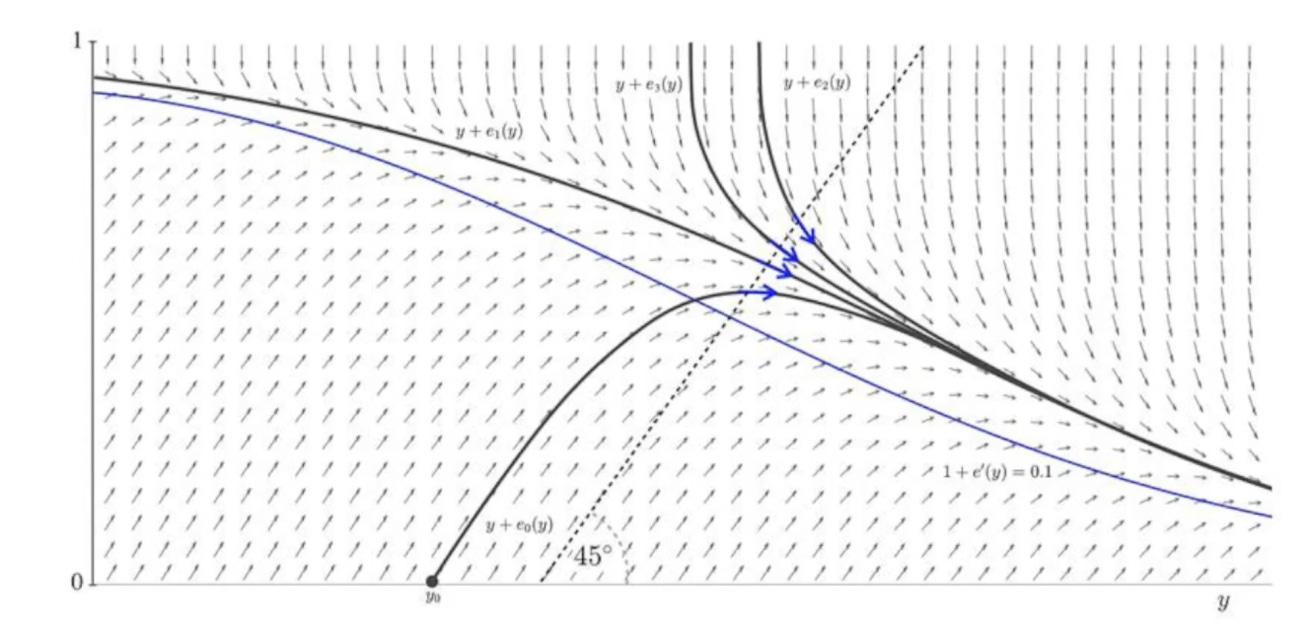

This prediction tells us that the more information is dispersed between providers, the more stable the TVL is and the calmer the agents will be. In the same manner, when more information is coordinated between agents, the more correlated it is and the more nervous agents are. This leads to an increase in the overall likelihood that agents will withdraw their liquidity and create instability.

This also means that scalability is a major tool for market stability. Scalability addresses both the need for depth of liquidity and the number of organic agents that dilute information.

Liquid lockers commit additional liquidity to the markets, through the emission of native tokens ruled by an internal decentralized governance layer. By deepening the available liquidity of assets, they contribute to the scalability of the ecosystem, as the issued tokens are paired together in the secondary markets.

As of today, the liquidity provided by Curve finance in CRV is net doubled by the incentives of Convex finance and Frax. Both of these DAOs extract value from fees and empower the synergy by relocking, permanently, the emission captured.

By using a governance framework based on LP tokens (such as BAL / 80-20 BPT) and distributing their underlying tokens as voting incentives, there is a way to create a much more aligned system than what is currently in place.

Governance tokens are the currency of the game, it is much more interesting to pay rewards in such format as it will create weekly buy pressure on CRV and BAL;

It is also highly likely most rewards are captured by liquid lockers who need these to grow;

With Quest, we could provide a custom interface where the reward / emission ratio is fixed to 1. This means that the briber would offer the highest reward while not “wasting” resources;

Liquid wrapper users could also vote on the Core Pool Quests as our platform is the only cross-layer vote incentive marketplace.