Weekly Gauge #11 : Real Yield & Revenues

DeFi has often been touted by naysayers and non-believers to be worthless as protocols would not create intrinsic value, calling them “ponzi” or “scams” (if you have doubts on what is a ponzi, read this). During the 2021 bull market, following the behavior of traditional central banks, many up and coming projects printed virtual value superior to their fundamental value. This behavior led to a snowball effect of short term incentives campaigns attracting a tidal wave of mercenary capital from retail and institutional investors.

Since the bear market is persisting, most of those tokens’ prices collapsed, lowering the market capitalization of underlying projects closer to revenue multiples. In the middle of this crypto crisis, some projects managed to keep their head above water and have been highlighted for their ability to justify their valuation with various revenue streams and well-designed tokenomics.

From here a new narrative called « Real Yield » is thriving. More than just a marketing spin, it shows the rising concern of the ecosystem to build sustainable and efficient business models to shape a better future of finance.

Real yield = Total Revenue – Operation Costs – Value of Total Token Emissions

One interesting way to align all stakeholders introduced by Curve Finance, and quickly reproduced by many other projects, is the veTokenomic.

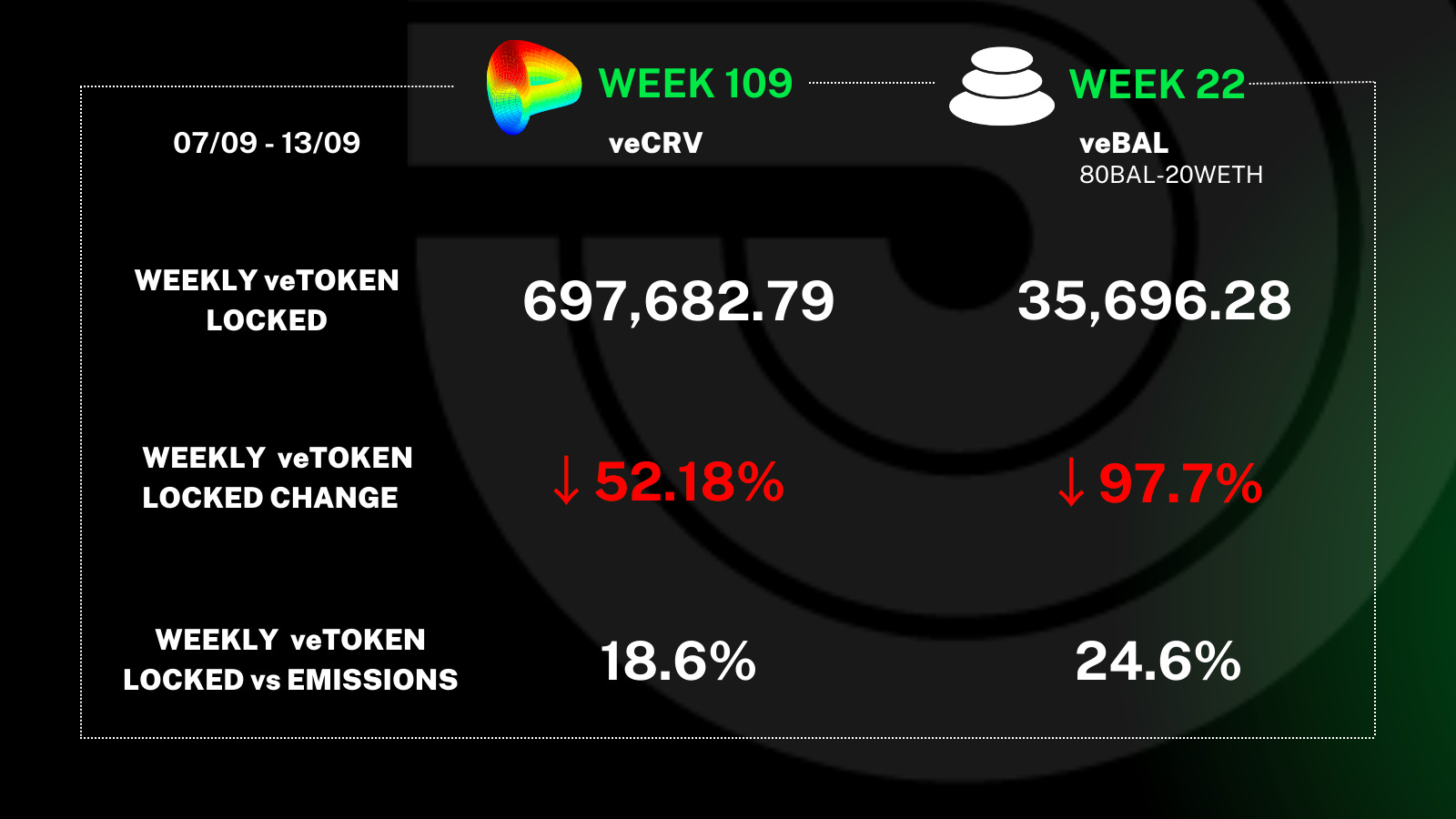

Balancer Week 22

BIP-57 ; Balancer Gauge Framework V1

While the first step toward this real yield narrative would be to direct the inflation of native tokens according to the share of revenue generated by each pool, Balancer decided to take a different path. They currently bootstrap the lock rate of BAL tokens, reducing the circulating supply, which then allows them to maintain a high emission rate (APY) without overvaluing it compared to the generated revenue.

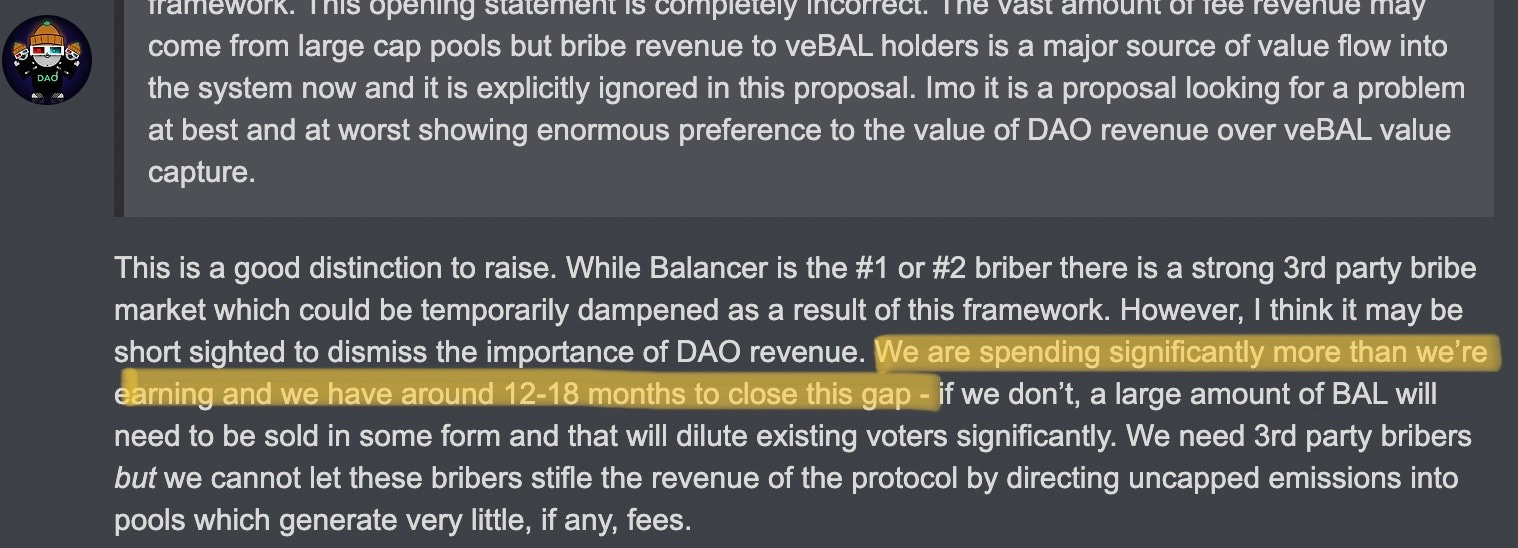

This strategy seemed to work well as the locked supply grew by several millions of tokens in a two months span. Unfortunately, the project faced an unexpected issue caused by the distribution of veBAL among its users and particularly the stake of one voter who directed the emission to pools generating very low incomes for the DAO.

On top of that, liquid lockers are potentially misaligned with the protocol’s focus on revenue. Given that 1 vlAURA controls around 0.3 veBAL we could expect the asset to yield only a third of it, in reality, vlAURA yields almost 80% more because AURA emissions are higher early on in the distribution.

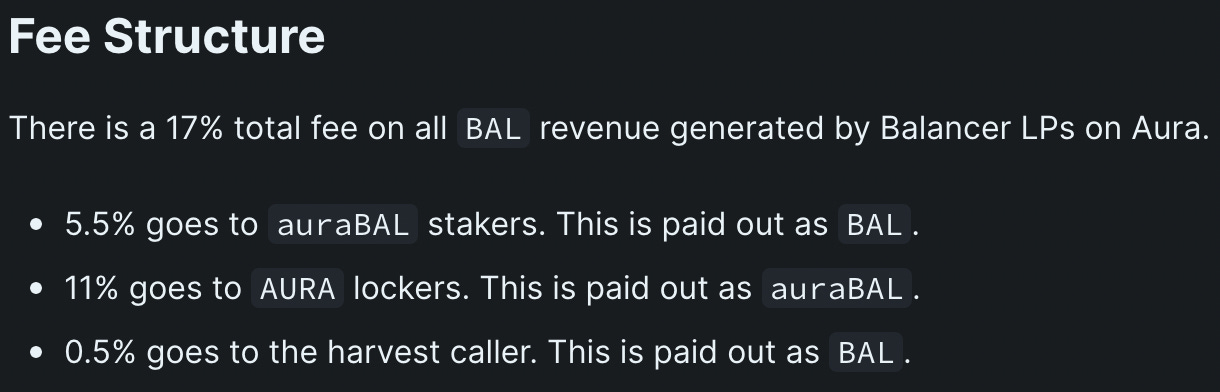

On the other hand, Aura Finance’s value proposition to add another layer of yield according to their share of Balancer’s revenue is ruled by the below formula and fee structure designed to match Aura’s inflation and their share of Balancer’s revenues and meet the real yield criteria (concept pioneered by Convex Finance).

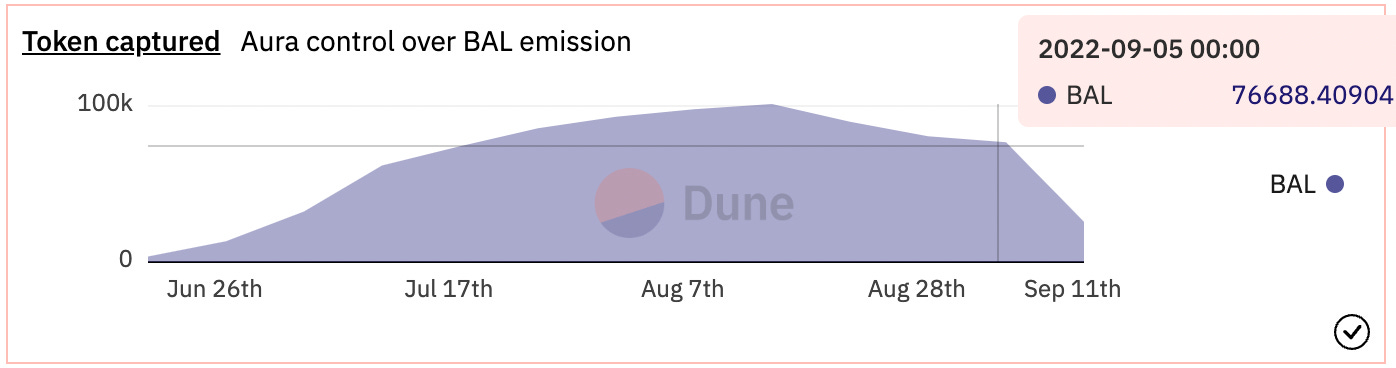

Moreover, the chart below indicates that half of BAL emission is captured by Aura protocol while they own roughly 23% of veBAL supply, this can justify the $ emission per vote difference between both protocols.

Balancer Governance Dashboard by Paladin

Curve Week 109

For the Curve ecosystem, Convex is a good example of what liquid lockers should aim for in terms of flywheel or symbiosis in value proposition on the DeFi stack as they capture more than 90% of CRV emission while owning around 50% of underlying veTokens.

Convex revenue share on CRV emission

Moreover, Convex has a really good understanding of how to allocate their delegated voting power among gauges and maintain a very accurate vote weight according to Curve pools’ revenues.

In conclusion, the real yield narrative is certainly a more accurate way to enhance the legitimacy of the DeFi ethos. It all relies on the ability of protocols to manage their incentive campaign according to what they actually create as intrinsic value.

Paladin.vote’s value proposition is completely driven by this thesis. Quest incentivises bribers to maintain sustainable ratios for all stakeholders based on the main revenue source of every protocol, which are collected fees.