Weekly Gauge #69 Aftermath of a long CRV story

Bullish Liquidation ?

What happened

Last week, Curve’s haters finally won the loan battle initiated by Evy and Mich’s loans collapsed.

Michael Egorov, known for his adept handling of high-stakes lending games in DeFi, has long thrived in the on-chain lending arena. Despite frequently borrowing close to liquidation thresholds, he had always managed to avoid forced liquidations. That’s how (and maybe why) LLAMMA soft liquidation mechanism was born.

However, on the 13th of June, the liquidation event started the infamous and long awaited "death spiral" for Curve through some vague sequence of events.

But what really happened?

In an interview with Cointelegraph, Egorov emphasized, “This was not a Curve exploit. This was an exploit of a separate project [UwU Lend],” explaining that the hacker, as part of their cash-out strategy, deposited CRV tokens taken from UwU Lend into LlamaLend and subsequently absconded with the funds, leaving the debt within the system. He advised UwU Lend to re-verify all contracts and engage reputable security auditors to help recover the losses and prevent future exploits.

Most of the lending platforms were not affected as they managed to liquidate the assets without any bad debt, that’s the case of Aave, Silo, Inverse and Frax. But LLAMA lend suffered about $10 million in bad debt. However two days after the event, Egorov announced that he had fully repaid bad debt caused by the soft liquidations resulting from the UwU exploit. He stated, “CRVs posted as collateral for loans amounted to probably 30% of the circulating supply; half of that was on Curve, so indeed, it incurred some bad debt. It was already repaid. No one is affected.”

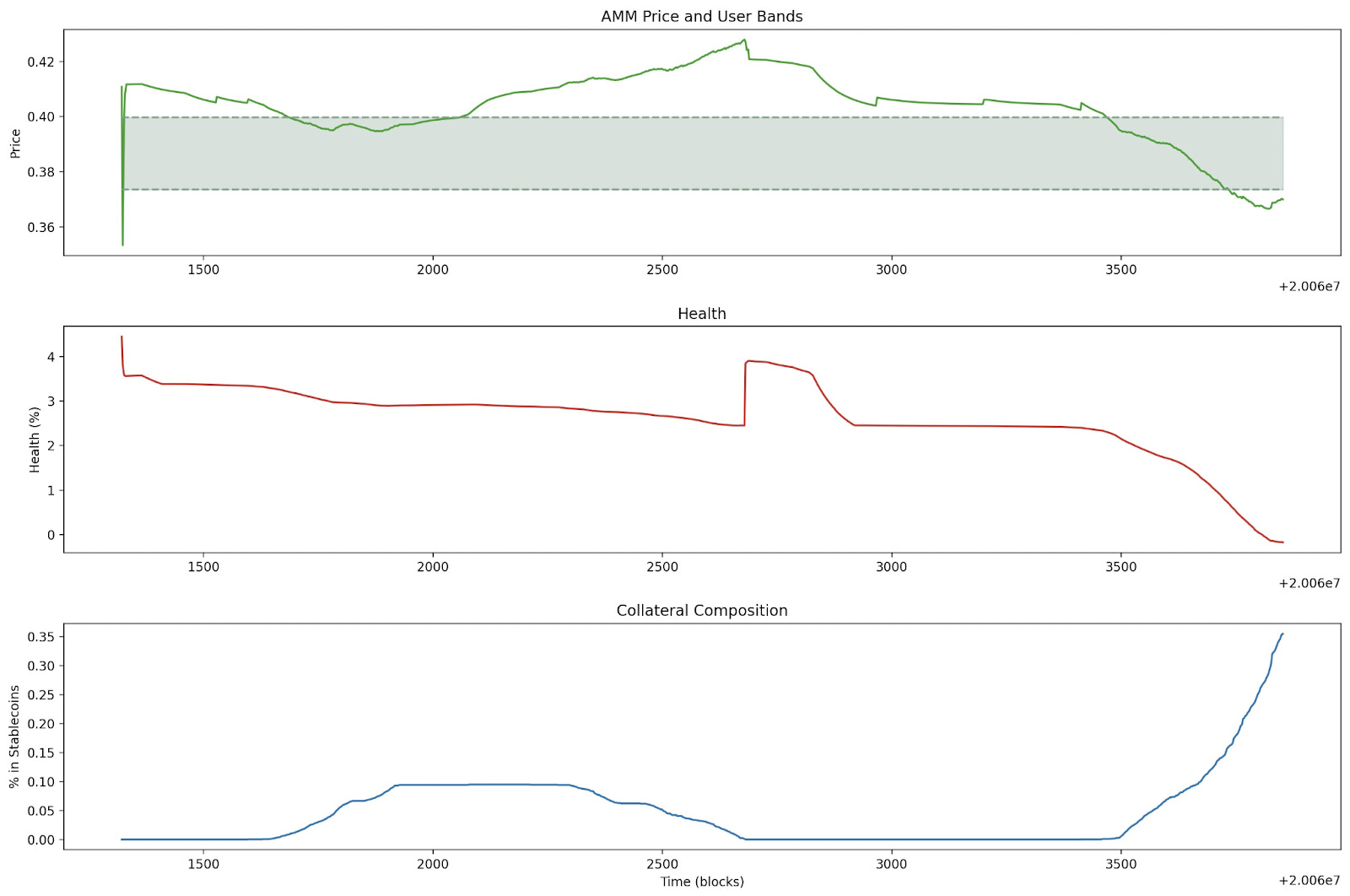

With the event came the big dump of CRV which went as low as $0.2 and that’s where everyone thought Curve was dead, because with the token price dropping it is the whole curve flywheel that is impacted as the emission and bribes are suddenly not really interesting anymore.

But was it really a “death spiral”?

But from what happened on chain, clearly there was exceptional strong demand at its lowest point. The demand in the low $0.20 range was particularly robust. Despite a market cap of $400 million, approximately $125 million (nearly 30% of the total market cap) was liquidated and quickly bought up within a 20% price range. This $125 million represented real money, not just theoretical market cap calculations. Such a significant liquidation, amounting to 30% of the market cap, would have likely been of synonym of death for any other protocol. But instead it was bought by many different actors acquiring cheap CRV from Mich himself. It wouldn’t be surprising to say that CRV probably bottomed out at $0.2.

https://x.com/Christianeth/status/1801195455461949826

What about the other metrics?

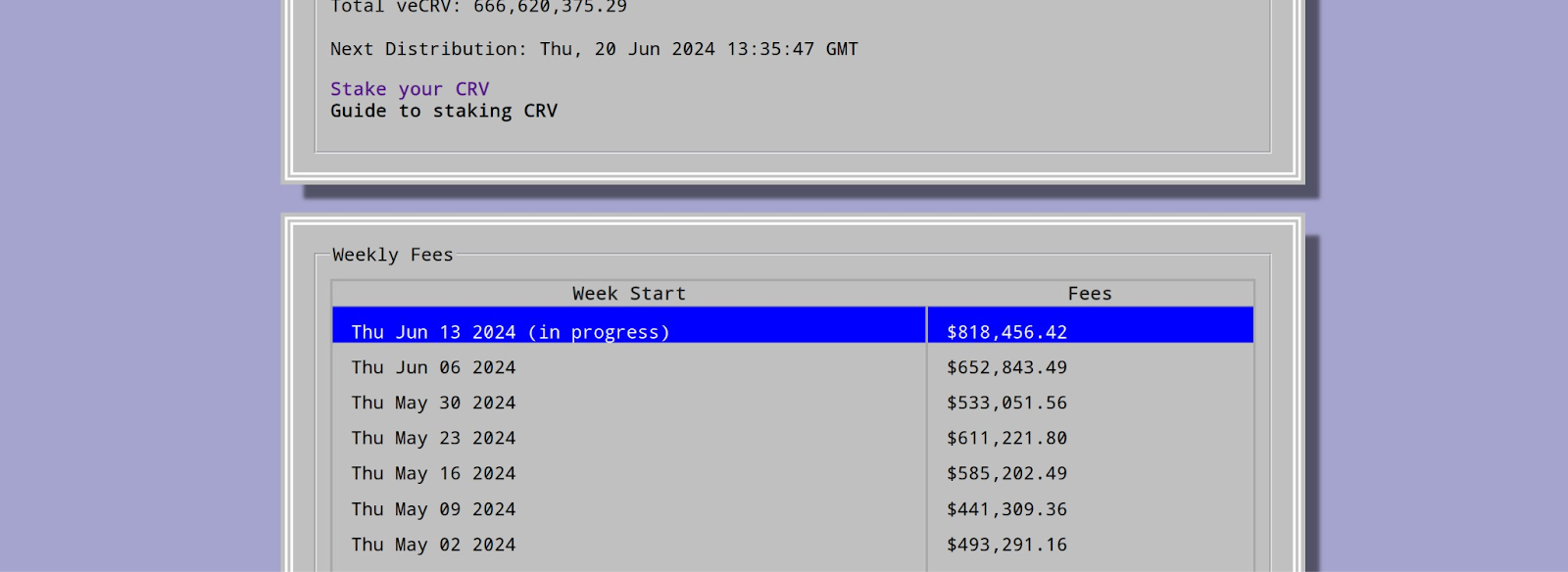

Whenever something bad happens in the DeFi landscape the fees generated by Curve are always through the roof. And this time is no different, thanks to the liquidation and volume trading, veCRV fees for the week are north of $800,000.

Curve DEX’s TVL has been stable despite the token's falling price over the past couple of months Users who remain are now less influenced by token price, the TVL is pretty sticky. Moreover Curve DEX is no longer the primary revenue generator since the introduction of crvUSD.

So what about the crvUSD, the recent events did cause crvUSD to experience its first significant upwards depeg, reaching as high as 1.07. However, this was short-lived as the protocol's mechanisms brought it back in line. crvUSD passed this stress test with ease, as it was designed to do. A depeg is a depeg but in people’s mind an upwards depeg feels way less dangerous than a downwards one because holders are literally just making a profit, however it denotes some little flaws in the mechanisms to maintain the peg and it can not be overlooked.

And finally for Llama Lend, the isolated markets meant potential bad news for the CRV long market accumulating bad debt. With a potential bad debt of up to $11 million it was a pretty bad situation, if it was not Mich’s position but someone else's it could have been way worse and endangered all the crvUSD suppliers of the market. It is worth noting that LLAMMA can both liquidate and de-liquidate, meaning a rise in CRV price could have restored the collateral's value, allowing suppliers to be repaid. But as mentioned earlier Mich has paid off all the bad debt at his own cost.

So what comes next?

About llama lend and the liquidation risks in volatile markets, the whole Curve team is working on a paper to try to resolve the soft liquidation issue. This event was kind of a huge stress test and the protocol will iterate based on the outcomes of such a situation. First, it is advisable to provide borrow caps. Michael noted that data indicates Curve-specific markets can be well-parameterized to handle such conditions. He also highlighted the importance of on-chain arbitrage and mentioned that the industry heavyweights were initially unsure how to manage the liquidations for his position on Curve, which led him to address it himself.

Looking ahead, Egorov suggested creating open-source liquidation bots and enhancing community education about liquidations to address broader decentralized finance implications.

How did the market react?

With Michael Egorov’s forced capitulation and liquidation now behind us and the bad debt in LlamaLend has been cleared, removing a significant obstacle, the path ahead for Curve appears promising.

Additionally, the upcoming emissions cut in August is set to further stabilize the market going from 20% down to only 6.5% inflation. This week alone, 20.5 million veCRV were locked, signaling strong community commitment. It is equivalent to locking about 8 weeks worth of emissions at current rates.

this was trans in the chart as CRV went back up to $0.35.

On the Convex front, CVX experienced a remarkable surge, more than doubling to $4.2 with record trading volumes on Binance.

Moreover, Convex announced the introduction of cvxNPR for the upcoming Pendle concurrent, adding another layer of bullish momentum. With these positive developments, the Curve flywheel seems poised for sustained growth and resilience.

Curve and Convex are still more alive than ever and some of the best cash flow assets in DeFi.